Email: chenlephuhai@gmail.com / 0904439939 / Địa chỉ: 252/68 D Lý Chính Thắng, Phường 9, Quận 3, TP.HCM.

Fixed Annuity Calculator Estimate Future Value

The future value of ordinary annuity calculator is used to implement the ordinary annuity. The present value of an annuity refers to how much money would be needed today to fund a series of future annuity payments. Or, put another way, it’s the sum that must be invested now to guarantee a desired payment in the comprehensive income future. Future value, on the other hand, is a measure of how much a series of regular payments will be worth at some point in the future, given a set interest rate. If you’re making regular payments on a mortgage, for example, calculating the future value can help you determine the total cost of the loan.

The Annuity Formula for the Present and Future Value of Annuities

It’s all simplified for you in this turn-key system that takes just 30 minutes per month. Because the growth of an annuity is tax-deferred, you will not need to worry about paying taxes on these annuities until later. If you continue making contributions, you can increase the value of your annuity. Note that the present annuity calculator can deal exclusively with fixed immediate annuities. Interest accrued during each period is added to the starting balance and compounds over time. Annuity.org is a licensed insurance agency in multiple states, and we have two licensed insurance agents on our staff.

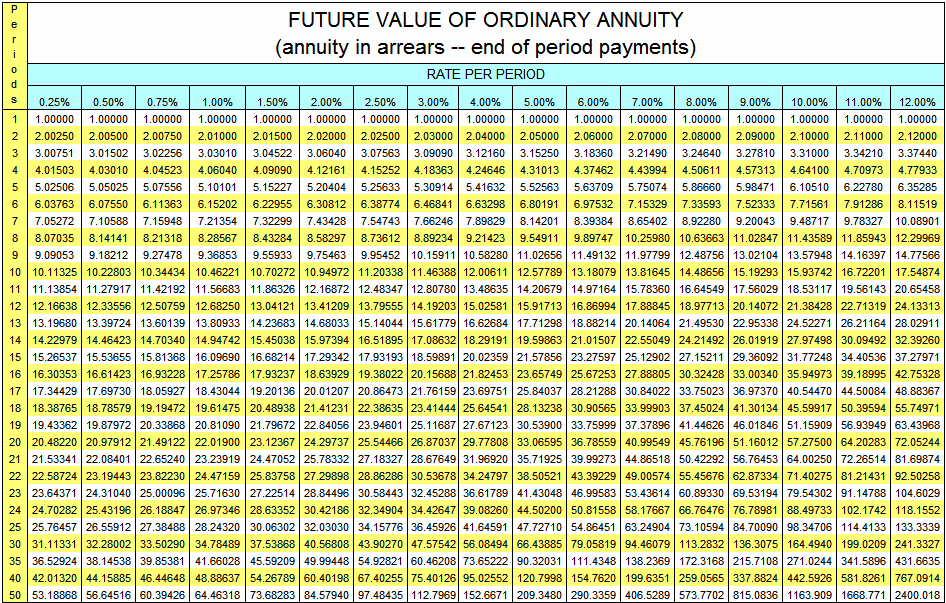

Using the TI BAII Plus Calculator to Find the Future Value for Ordinary Annuities

For an example calculation, let’s use the same parameters as the previous example but for an Annuity Due. Investing $100 at the beginning of each month for 10 years at an annual interest rate of 5%, compounded monthly. This small change will result in a slightly higher future value compared to the Ordinary Annuity, reflecting the additional compounding period for each payment. Practically anyone planning for the future—whether it’s saving for retirement, education funds, or managing long-term financial investments. Financial advisors use it to provide clients with precise future value estimates, ensuring that financial plans are robust and realistic.

One Month After the Rate Cut: Where Are Annuity and Other Interest Rates Now?

We are compensated when we produce legitimate inquiries, and that compensation helps make Annuity.org an even stronger resource for our audience. We may also, at times, sell lead data to partners in our network in order to best connect consumers to the information they request. Readers are in no way obligated to use our partners’ services to access the free resources on Annuity.org. The easiest way to understand the difference between these types of annuities is to consider a simple example. Let’s assume that you deposit 100 dollars annually for three years, and the interest rate is 5 percent; thus, you have a $100, 3-year, 5% annuity.

2 Future Value of Annuities

There are several ways to measure the cost of making such payments or what they’re ultimately worth. Read on to learn how to calculate the present value (PV) or future value (FV) of an annuity. This explains why annuity amounts (cash flows) can be referred to as deposits and payments at the same time. An Annuity Due indicates payments are received at the beginning of each period, whereas an Ordinary Annuity indicates payments are received at the end of each period.

Together with the figures explained in the above, this calculator displays a details report showing the growth per each period. Immediate annuities for senior citizens tend to be the best annuities for seniors because they begin paying out within 12 months of purchase. “Essentially, a sum of money’s value depends on how long you must wait to use it; the sooner you can use it, the more valuable it is,” Harvard Business School says. A lower discount rate results in a higher present value, while a higher discount rate results in a lower present value. So, let’s assume that you invest $1,000 every year for the next five years, at 5% interest. Follow me on any of the social media sites below and be among the first to get a sneak peek at the newest and coolest calculators that are being added or updated each month.

When the calculator is in annuity due mode, a tiny BGN appears in the upper right-hand corner of your calculator. When the calculator is in ordinary annuity mode there is nothing in the upper right-hand corner. The steps required to solve the future value of an annuity due are identical to those you use for an ordinary annuity except you use the formula for the future value of an annuity due. When we are utilizing the future value of an annuity calculator, we are going to find the detailed output of annuity.

- So if you have a question about the calculator’s subject, please seek out the help of someone who is an expert in the subject.

- In summary, understanding and accurately calculating the Future Value of Annuities is fundamental in financial planning.

- It is important for each individual to evaluate their specific situations or consult professionals.

- Unlike spreadsheets and financial calculators, there is no convention of negative numbers in our future value of annuity calculator and only positive values must be entered.

An investor who wants to balance risk with growth potential might want to look at the projected growth of a fixed annuity alongside that of an indexed or variable annuity. These other types of annuities may not offer the same guaranteed returns as a fixed annuity, but their potential for gains tends to be higher. There are different examples of annuities like savings accounts, monthly mortgage payments, and pension payments. The future value of an annuity calculator is adjustable for finding the annuity for any time period regardless of whether we are calculating on a daily, monthly, or yearly basis. In many cases, investors will start with an initial amount and make additional investments over time. For example, an investor may start with a $100,000 annuity and contribute an additional $10,000 yearly until they retire.

The amount paid for or the principal amount around which we are doing the compounding. We can find it by dividing the interest rate by 100 as it is described as 5% or 6% etc. The future value of the annuity calculator automatically converts the values of “i” by dividing it by 100. The value calculated by the ordinary annuity calculator is $ 5,525.64 after 5 years and an interest rate of 5 %.